Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Thank You for All of Your Support

There’s no denying the long-term financial benefits of owning a home, but today’s housing market may have you wondering if now’s still the time to buy. While the financial aspects of buying a home are important, the non-financial and emotional reasons are too.

Home means something different to all of us. Whether it’s sharing memories with loved ones at the kitchen table or settling in to read a book in a favorite chair, the emotional connections to our homes can be just as important as the financial ones. Here are some of the things that make a house a home.

1. You Can Be Proud of Your Accomplishment

Buying a home is a major life milestone. Whether you’re setting out to buy your first home or your fifth, congratulations will be in order when you’ve achieved your goal. The sense of accomplishment you’ll feel at the end of your journey will truly make your home feel like a special place.

2. You Have Your Own Designated Happy Place

Owning your own home offers not only safety and security, but also a comfortable place where you can relax and unwind after a long day. Sometimes that’s just what you need to feel recharged and content.

3. You Can Find the Space To Meet Your Needs

Whether you want more room for your changing lifestyle (like retirement, dedicated space for a hobby, or a personal gym) or you simply prefer to have a large backyard for entertaining, you can invest in a home that truly works for your evolving needs.

4. You Can Customize Your Surroundings

Looking to try one of those decorative wall treatments you saw online? Tired of paying an additional pet deposit for your apartment building? Or maybe you want to create an in-home yoga studio. You can do all these things in your own home.

Bottom Line

Whether you’re planning to purchase your first home or you’re ready to buy a different home to meet your needs, consider the emotional benefits that can turn a house into a happy home. When you’re ready to make a move, let’s connect.

The 2022 housing market has been defined by two key things: inflation and rapidly rising mortgage rates. And in many ways, it’s put the market into a reset position.

As the Federal Reserve (the Fed) made moves this year to try to lower inflation, mortgage rates more than doubled – something that’s never happened before in a calendar year. This had a cascading impact on buyer activity, the balance between supply and demand, and ultimately home prices. And as all those things changed, some buyers and sellers put their plans on hold and decided to wait until the market felt a bit more predictable.

But what does that mean for next year? What everyone really wants is more stability in the market in 2023. For that to happen we’ll need to see the Fed bring inflation down even more and keep it there. Here’s what housing market experts say we can expect next year.

Moving forward, experts agree it’s still going to be all about inflation. If inflation is high, mortgage rates will be as well. But if inflation continues to fall, mortgage rates will likely respond. While there may be early signs inflation is easing as we round out this year, we’re not out of the woods just yet. Inflation is still something to watch in 2023.

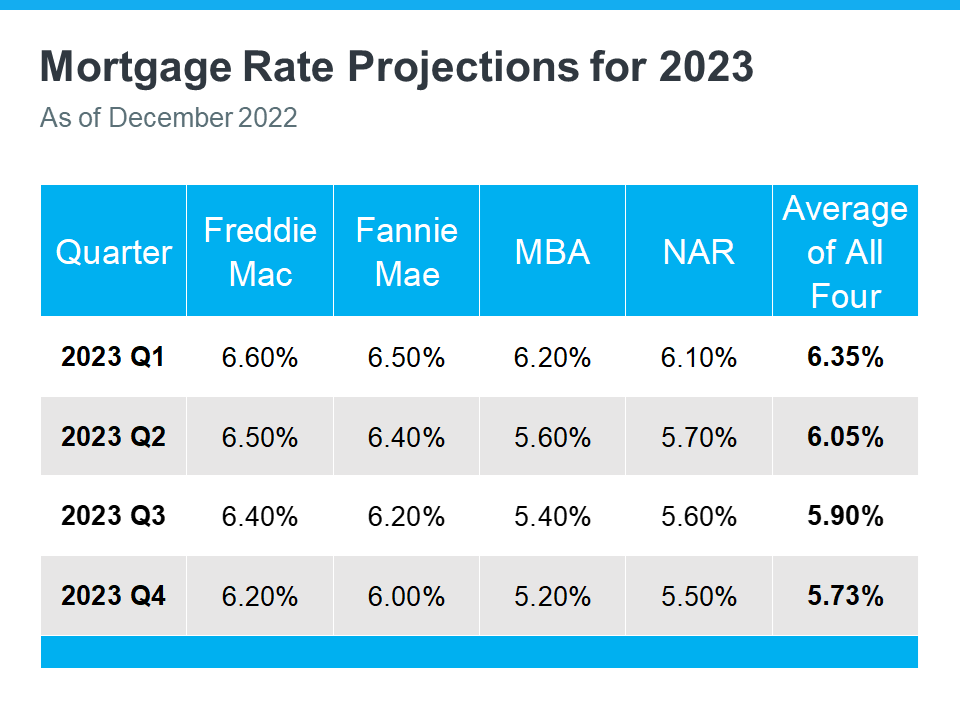

Right now, experts are factoring all of this into their mortgage rate forecasts for next year. And if we average those forecasts together, experts say we can expect rates to stabilize a bit more in 2023. Whether that’s between 5.5% and 6.5%, it’s hard for experts to say exactly where they’ll land. But based on the average of their projections, a more predictable rate is likely ahead (see chart below):

That means, we’ll start the year out about where we are right now. But we could see rates tick down if inflation continues to drop. As Greg McBride, Chief Financial Analyst at Bankrate, explains:

“. . . mortgage rates could pull back meaningfully next year if inflation pressures ease.”

In the meantime, expect some volatility as rates will likely fluctuate in the weeks ahead. If we see inflation come back under control, that would be good news for the housing market.

Homes prices will always be defined by supply and demand. The more buyers and fewer homes there are on the market, the more home prices will rise. And that’s exactly what we saw during the pandemic.

But this year, things changed. We’ve seen home prices moderate and housing supply grow as buyer demand pulled back due to higher mortgage rates. The level of moderation has varied by local area – with the biggest changes happening in overheated markets. But do experts think that will continue?

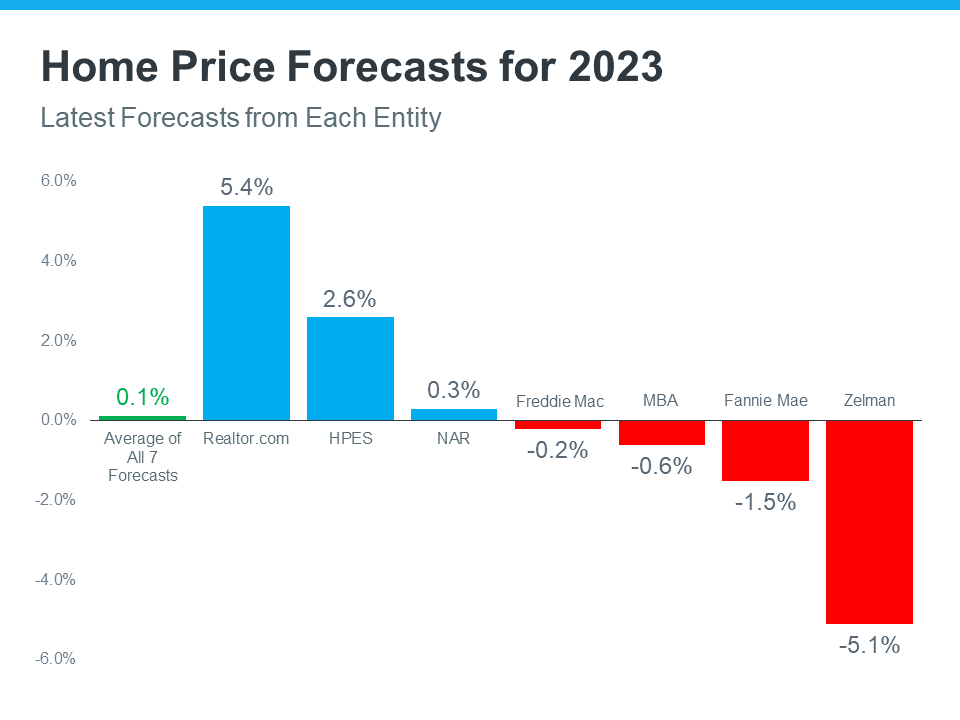

The graph below shows the latest home price forecasts for 2023. As the different colored bars indicate, some experts are saying home prices will appreciate next year, and others are saying home prices will come down. But again, if we take the average of all the forecasts (shown in green), we can get a feel for what 2023 may hold.

The truth is probably somewhere in the middle. That means nationally, we’ll likely see relatively flat or neutral appreciation in 2023. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“After a big boom over the past two years, there will essentially be no change nationally . . . Half of the country may experience small price gains, while the other half may see slight price declines.”

The 2023 housing market is going to be defined by mortgage rates, and rates will be determined by what happens with inflation. The best way to keep a pulse on what experts are projecting for next year is to lean on a trusted real estate advisor. Let’s connect.

If you’re a homeowner, your net worth got a big boost over the past few years thanks to rapidly rising home prices. Here’s how it happened and what it means for you, even as the market moderates.

Equity is the current value of your home minus what you owe on the loan.

Because there was a significant imbalance between the number of homes available for sale and the number of buyers looking to make a purchase over the past few years, home prices appreciated substantially.

And while home price appreciation has moderated this year, and even depreciated slightly in some overheated markets, that doesn’t mean you’ve lost all the equity you gained during the pandemic frenzy.

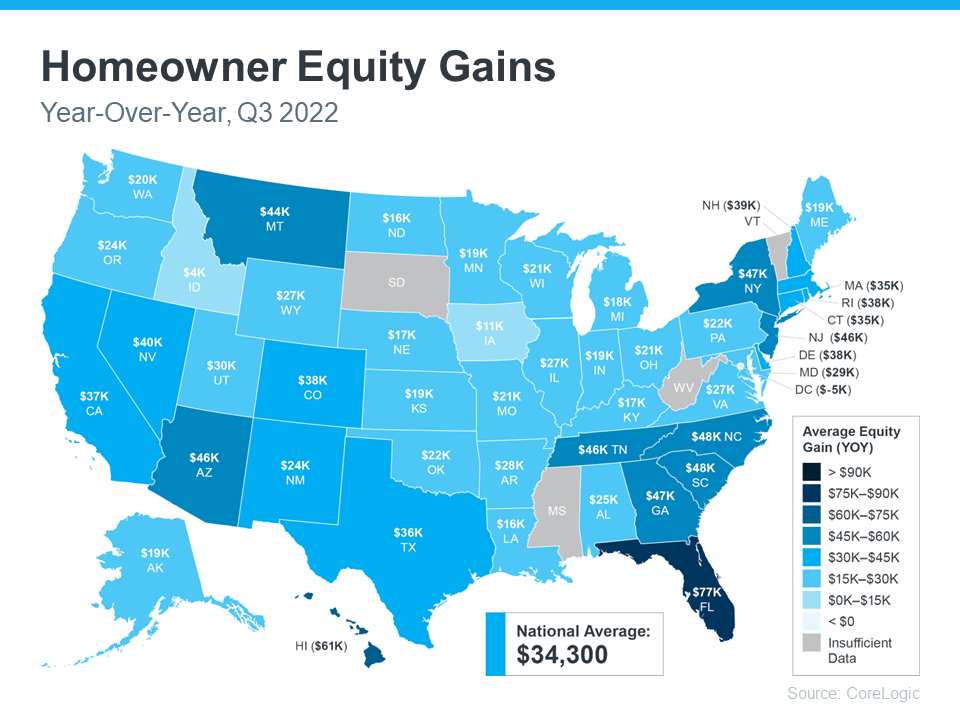

To prove you still have equity you can use, the latest Homeowner Equity Insights from CoreLogic finds the average homeowner equity has actually grown by $34,300 over the past 12 months.

That’s right, despite the headlines, the average homeowner still gained positive equity over the last year in just about every market. While the gains aren’t as dramatic as they were in the previous quarter due to home price moderation, they’re still significant. And if you’ve been in your home for longer than a year, chances are you have even more equity than you realize.

While that’s the national number, if you want to know what happened over the past year in your area, look at the map below from CoreLogic:

While equity helps increase your overall net worth, it can also help you achieve other goals, like buying your next home. When you sell your current house, the equity you’ve built up comes back to you in the sale, and it may be just what you need to cover a large portion – if not all – of the down payment on your next home.

So, if you’ve been holding off on selling because you weren’t sure what the headlines meant for your bottom line, rest assured you’ve still gained equity in recent years, and it can help fuel your move.

If you’re planning to make a move, the equity you’ve gained over time can make a big impact. To find out just how much equity you have in your current home and how you can use it to fuel your next purchase, let’s connect.

![2023 Housing Market Forecast [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/12/15125347/2023-Housing-Market-Forecast-MEM-1046x2665.png)

Planning to Retire? It Could Be Time To Make a Move.

Planning to Retire? It Could Be Time To Make a Move. | MyKCM

If you’re thinking about retirement or have already retired this year, you may be planning your next steps. One of your goals could be selling your house and finding a home that more closely fits your needs.

Fortunately, you may be in a better position to make a move than you realize. Here are a few things to think about when making that decision.

Consider How Long You’ve Been in Your Home

From 1985 to 2008, the average length of time homeowners typically stayed in their homes was only six years. But according to the National Association of Realtors (NAR), that number is rising today, meaning many homeowners are living in their houses even longer (see graph below):

Planning to Retire? It Could Be Time To Make a Move. | MyKCM

When you live in a home for a significant period of time, it’s natural for you to experience a number of changes in your life while you’re in that house. As those life changes and milestones happen, your needs may change. And if your current home no longer meets them, you may have better options waiting for you.

Consider the Equity You’ve Gained

Additionally, if you’ve been in your home for more than a few years, you’ve likely built up significant equity that can fuel your next move. That’s because the longer you’ve been in your home, the more likely it’s grown in value due to home price appreciation. Data from the Federal Housing Finance Agency (FHFA) illustrates that point (see graph below):

Planning to Retire? It Could Be Time To Make a Move. | MyKCM

While home price growth varies by state and local area, the national average shows the typical homeowner who’s been in their house for five years saw it increase in value by over 50%. And the average homeowner who’s owned their home for 30 years saw it almost triple in value over that time.

Consider Your Retirement Goals

Whether you’re looking to downsize, relocate to a dream destination, or move so you live closer to loved ones, that equity can help you achieve your homeownership goals. NAR shares that for recent home sellers, the primary reason to move was to be closer to loved ones. Plus, retirement played a large role for those moving greater distances.

Whatever your home goals are, a trusted real estate advisor can work with you to find the best option. They’ll help you sell your current house and guide you as you buy the home that’s right for you and your lifestyle today.

Bottom Line

Retirement can bring about major changes in your life, including what you need from your home. Let’s connect to explore your opportunities in our local market.

At first glance, the increase in housing supply compared to last year may not sound like good news for prospective sellers, but it actually gives you two key opportunities in today’s housing market.

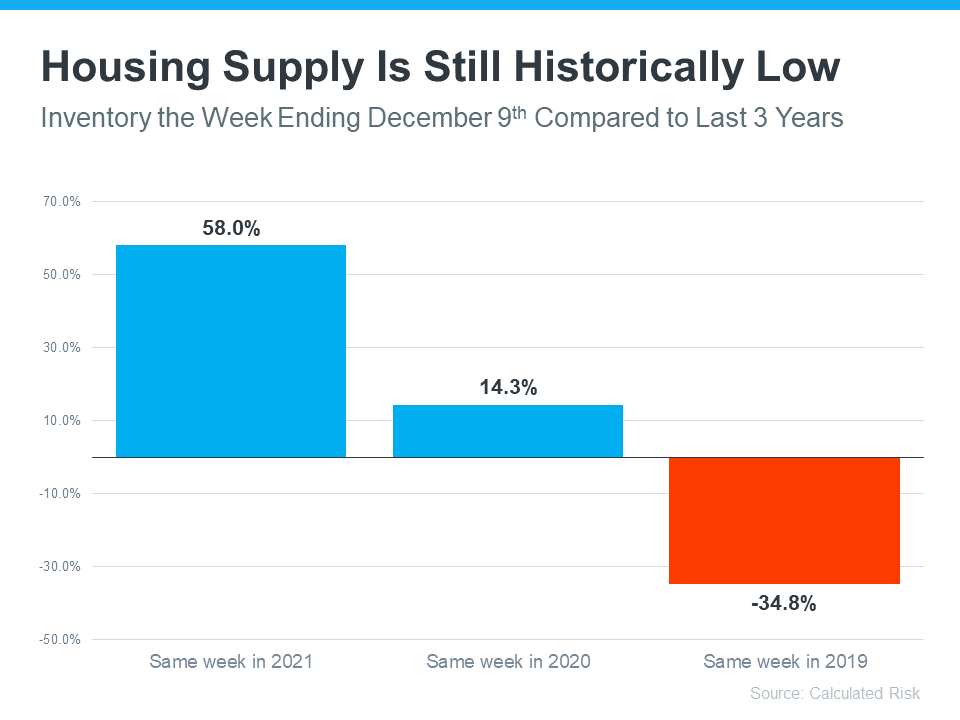

An article from Calculated Risk helps put the inventory gains the market has seen in 2022 into perspective by comparing it to recent years (see graph below). It shows supply has surpassed 2021 levels by 58%. But the further back you look, the more you’ll understand the bigger picture. And if you go all the way back to 2019, the last normal year in real estate, we’re roughly 35% below the housing supply we had at that time.

If your current house no longer meets your needs or lacks the space and features you want, this inventory growth gives you even more opportunity to sell and move into the home of your dreams. With more houses on the market, you’ll have more to choose from when you search for your next home.

Partnering with a local real estate professional can help you make sure you’re up to date on the homes available in your area. And when you do find the one, a professional can advise you on how to write a winning offer.

But again, despite the growth, inventory is still low compared to more normal years, and that isn’t going to change overnight. For you, that means your house should still be in demand among potential buyers if you price it right.

As an article from realtor.com says:

“Today’s shoppers generally have more homes to consider than last year’s shoppers did, but the market is still not back to pre-pandemic inventory levels.”

If you’re a homeowner looking to sell, you have more homes to choose from and can still sell your house while inventory is low overall. Let’s connect to get started, so you can have the best of both worlds.

If you’re trying to decide whether or not to sell your house, recent headlines about home prices may be top of mind. And if those stories have you wondering what that means for your home’s value, here’s what you really need to know.

It’s possible you’ve seen news stories mentioning a drop in home values or home price depreciation, but it’s important to remember those headlines are designed to make a big impression in just a few words. But what headlines aren’t always great at is painting the full picture.

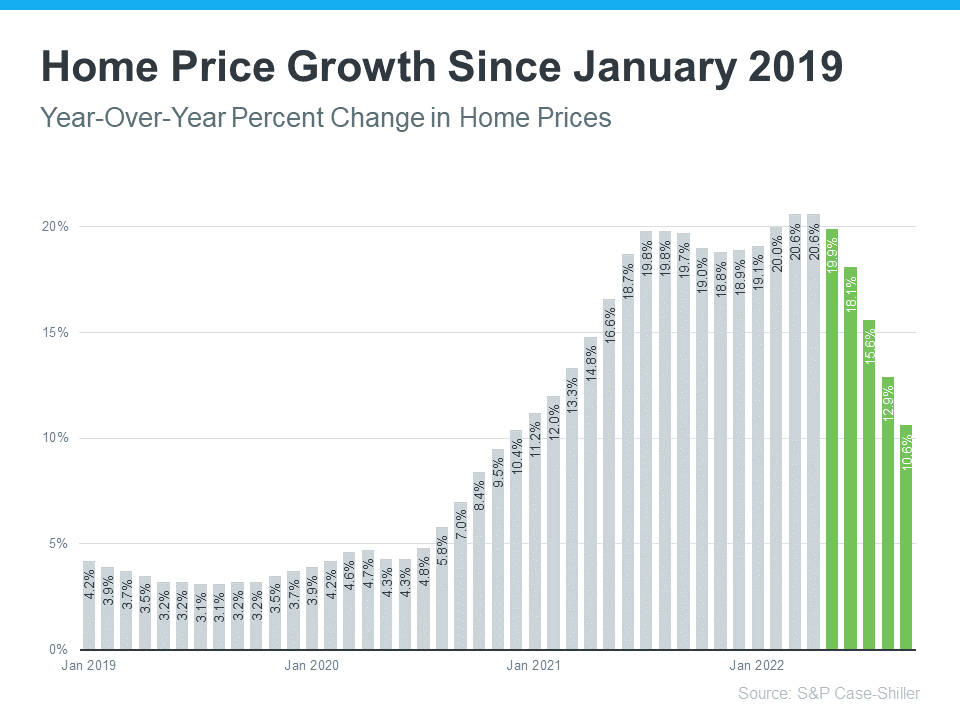

While home prices are down slightly month-over-month in some markets, it’s also true that home values are up nationally on a year-over-year basis. The graph below uses the latest data from S&P Case-Shiller to help tell the story of what’s actually happening in the housing market today:

As the graph shows, it’s true home price growth has moderated in recent months (shown in green) as buyer demand has pulled back in response to higher mortgage rates. This is what the headlines are drawing attention to today.

But what’s important to notice is the bigger, longer-term picture. While home price growth is moderating month-over-month, the percent of appreciation year-over-year is still well above the home price change we saw during more normal years in the market.

The bars for January 2019 through mid-2020 show home price appreciation around 3-4% a year was more typical (see bars for January 2019 through mid-2020). But even the latest data for this year shows prices have still climbed by roughly 10% over last year.

While you may not be able to capitalize on the 20% appreciation we saw in early 2022, in most markets your home’s value, on average, is up 10% over last year – and a 10% gain is still dramatic compared to a more normal level of appreciation (3-4%).

The big takeaway? Don’t let the headlines get in the way of your plans to sell. Over the past two years alone, you’ve likely gained a substantial amount of equity in your home as home prices climbed. Even though home price moderation will vary by market moving forward, you can still use the boost your equity got to help power your move.

As Mark Fleming, Chief Economist at First American, says:

“Potential home sellers gained significant amounts of equity over the pandemic, so even as affordability-constrained buyer demand spurs price declines in some markets, potential sellers are unlikely to lose all that they have gained.”

If you have questions about home prices or how much equity you have in your current home, let’s connect so you have an expert’s advice.

![Reasons To Sell Your House This Season [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/12/08121045/Reasons-To-Sell-Your-House-This-Season-MEM-1046x2601.png)

There are many people thinking about buying a home, but with everything affecting the economy, some are wondering if it’s a smart decision to buy now or if it makes more sense to wait it out. As Bob Broeksmit, President and CEO of the Mortgage Bankers Association (MBA), explains:

“The desire for homeownership is strong. Many prospective buyers are waiting for the volatility in mortgage rates to subside, as well as for a clearer picture of the economic outlook.”

If you’re in that position, remember that it’s important to consider not just what’s happening today but also what benefits you may gain in the long run.

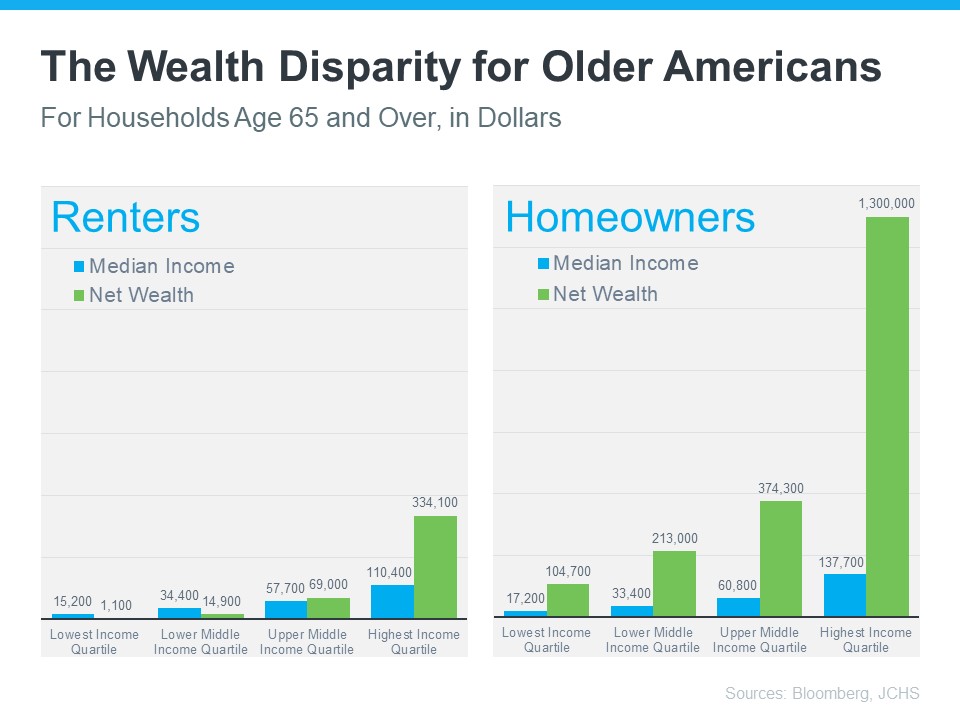

There’s a lot of information out there about how homeownership helps build a homeowner’s net worth over time. But even today, many people think first about things like 401(k)s before they think of owning a home as a wealth-building tool. It’s especially important if you’re a young prospective homebuyer to understand how homeownership is another key way to invest in your future. An article from Bloomberg notes:

“Millennials have higher average 401(k) balances than Generation X did when they were the same age, but they’re not any better off financially. . . . A lot of that has to do with being less likely to own a home.”

To help you understand just how much owning a home can have a positive impact on your life over the years, take a look at what the data shows. The same Bloomberg article helps show the gap in wealth between renters and homeowners who are 65 years and older (see graph below). The difference is substantial, even when incomes are similar.

So, if you want to create wealth to help set you up for success later on, it may be time to prioritize homeownership. That’s because, whether you decide to rent or buy a home, you’ll have a monthly housing expense either way. The question is: are you going to invest in yourself and your future, or will you help someone else (your landlord) increase their wealth?

Before putting your homeownership plans on hold, let’s connect to go over your options. That way, you’ll have expert advice on how to make the best decision right now and the best investment in your future.

© 2022 Coldwell Banker Realty